(Bloomberg) — Stocks struggled near their all-time highs ahead of the Federal Reserve rate decision, with traders split on the size of a central bank cut.

The S&P 500 was little changed after briefly crossing the threshold of its record amid a surprise increase in US retail sales. Treasury yields edged up, with shorter maturities leading the move. The market-implied odds that policymakers announce a 50-basis-point rate reduction on Wednesday were around 55%. Traders have fully priced in a full quarter-point worth of easing.

A survey conducted by 22V Research showed that expectations for the market reaction to the Fed decision are dependent on expectations for the size of the cut. Investors who expect a 25 basis-point cut are split on whether that cut will deliver a “risk-on” or “risk-off” reaction. Investors who expect a 50 basis-point reduction cut think a smaller cut will have a “risk-off” market reaction.

The Fed will either cut 50 basis points or opt for a 25 basis-point reduction, but signal that they will be more aggressive going forward, according to Matt Maley at Miller Tabak.

Still, he says, that does not guarantee that the stock market and/or bond market will rally in a meaningful way. Maley says the Fed will likely try to convey that a more dovish stance is not seen as something that means they’re suddenly worried about an imminent recession.

“Therefore, given that the stock market is approaching overbought territory, we could still get a ‘sell the news’ reaction to the Fed this week,” he added.

The S&P 500 hovered near 5,630. The Nasdaq 100 was little changed. The Dow Jones Industrial Average fluctuated. The Russell 2000 of smaller firms gained 0.8%. Treasury 10-year yields advanced three basis points to 3.65%. The dollar rose.

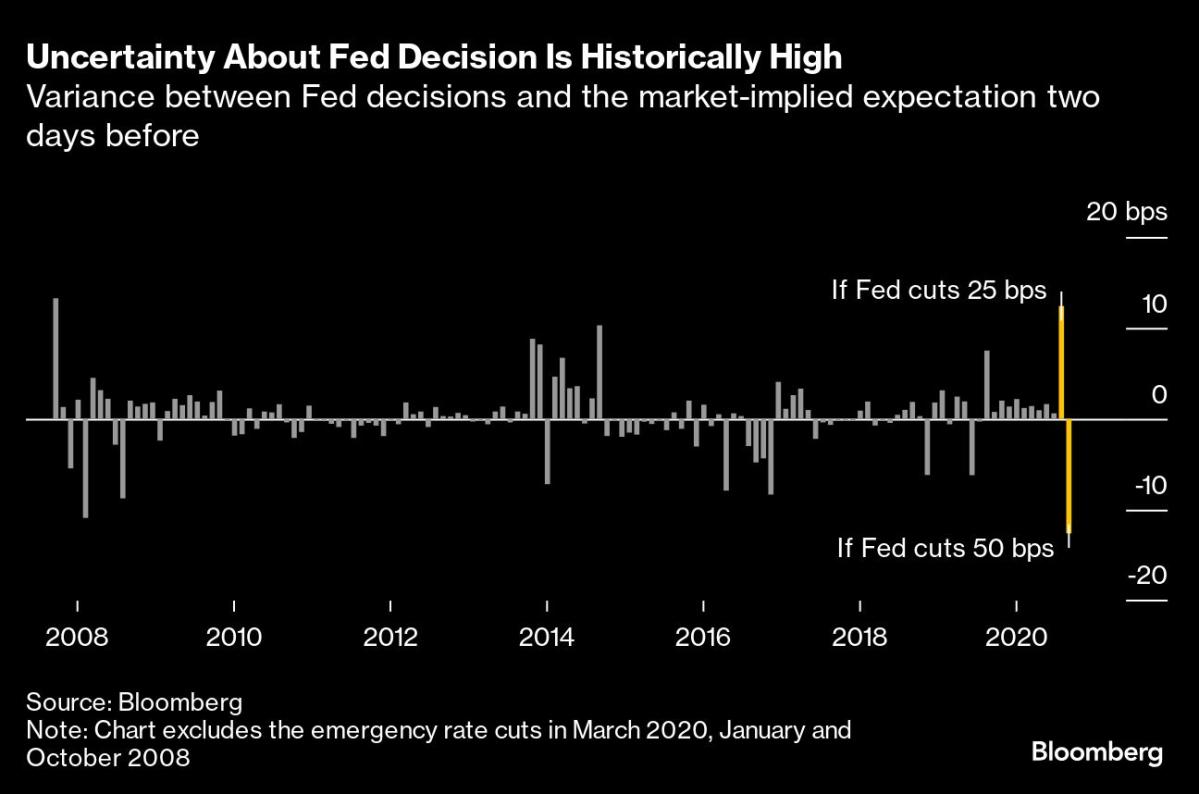

Right or wrong, market expectations were already shifting toward a 50 basis point Fed cut this week, according to Chris Larkin at E*Trade from Morgan Stanley.

“The stronger-than-anticipated headline retail sales number seemed to support that outlook, but the report’s fine print presented a more mixed picture,” Larkin said. “This data isn’t going to decide the issue for the Fed, one way or the other.”

That said, we’re not out of the woods quite yet, according to Bret Kenwell at eToro.

“There are reasons to be concerned about the labor market, and while the consumer is holding on enough to beat economists’ expectations, the results are not necessarily pointing to a consumer that is thriving,” he said.

The US economy remains on track for a soft landing, and the recent economic data are consistent with our view that the recession fears that triggered the early August selloff were overdone, according to Solita Marcelli at UBS Global Wealth Management.

“While we believe equity gains will broaden out, we also think there is room for growth stocks, in particular technology stocks, to rise further,” she said.

Marcelli also noted that while Fed rate cuts in non-recessionary periods have historically been favorable for equities overall, they also make growth stocks more attractive as lower rates increase the present value of these companies’ future cash flows.

Corporate Highlights:

- Microsoft Corp. raised its quarterly dividend 10% and unveiled a new $60 billion stock-buyback program, matching the size of a repurchase plan three years ago.

- Intel Corp. made a raft of announcements, spurring optimism that the chipmaker’s turnaround plan is starting to bear fruit.

- Newmont Corp., the world’s biggest gold miner, said it’s on track to raise $2 billion — if not more — from selling smaller mines and development projects.

- Reckitt Benckiser Group Plc has started early discussions with some of the potential suitors for its homecare assets, which could fetch more than £6 billion ($7.9 billion) in a deal, according to people familiar with the matter.

- Continental AG is pushing ahead with preparations for a separation of its struggling car parts business, even as it grapples with recalls related to faulty braking systems it supplied, according to people familiar with the matter.

Key events this week:

- Eurozone CPI, Wednesday

- Fed rate decision, Wednesday

- UK rate decision, Thursday

- US US Conf. Board leading index, initial jobless claims, US existing home sales, Thursday

- FedEx earnings, Thursday

- Japan rate decision, Friday

- Eurozone consumer confidence, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 was little changed as of 1:28 p.m. New York time

- The Nasdaq 100 was little changed

- The Dow Jones Industrial Average was little changed

- The MSCI World Index was little changed

- The Russell 2000 Index rose 0.8%

Currencies

- The Bloomberg Dollar Spot Index rose 0.2%

- The euro fell 0.1% to $1.1117

- The British pound fell 0.5% to $1.3156

- The Japanese yen fell 0.9% to 141.89 per dollar

Cryptocurrencies

- Bitcoin rose 5.7% to $60,948.16

- Ether rose 4.4% to $2,374.08

Bonds

- The yield on 10-year Treasuries advanced three basis points to 3.64%

- Germany’s 10-year yield advanced two basis points to 2.14%

- Britain’s 10-year yield advanced one basis point to 3.77%

Commodities

- West Texas Intermediate crude rose 2.2% to $71.60 a barrel

- Spot gold fell 0.6% to $2,565.93 an ounce

This story was produced with the assistance of Bloomberg Automation.

©2024 Bloomberg L.P.

Shared by Golden State Mint on GoldenStateMint.com