President Trump has announced a swathe of tariffs that he hopes will fund income tax cuts and incentivize manufacturing reshoring. In the long run it may deliver positives for the US economy, but the measures taken mean a painful transition period ahead.

Average tariff rate appears higher than expected

Donald Trump’s enthusiasm for tariffs is well known. He describes them as “the most beautiful word in the dictionary.” He sees them as a tool for achieving multiple objectives: a way of raising tax revenue, a way to incentivize reshoring of manufacturing to the US, and a diplomatic weapon to force a change of behaviors.

Having already used threats of tariffs on Canada and Mexico to shore up international borders, today’s announcement is focused on raising taxes and championing US manufacturing.

The details show a 10% base tariff for everyone, but then clear discrimination amongst countries that have, to a varying degree, been perceived to have cheated America. China gets 34%, Vietnam gets 46%, while the EU gets 20%. There is still some confusion on what Canada and Mexico are facing – it could be 25%, it could be zero. Proxying the top 20 of trade partners (contributing 85% of imports into the US), depending on what happens with Canada and Mexico this works out as being in an 18.5-26.5% tariff.

For now, we are assuming this equates to around $600bn of tariffs.

Average tariff on US imports

ING assumption for 2025

Long-term benefits may come, but near-term pain looks certain

Today’s actions make the argument for reshoring at least some activity to the US much stronger. However, US manufacturing wages are amongst the highest in the world – the National Association of Manufacturers states that in 2023, manufacturing employees earned an average of $102,629, including pay and benefits. For China, it is around 25%, and for Korea, it is around 40% of that figure. Even in Germany, it is less than 75% of the US figure. This suggests that it would only make sense to reshore activity related to highly automated, high skill, high value-added production or for products where there is a strong market that consumers are willing to pay a premium for a ‘Made in America’ label.

Given the costs of moving production to the US many other manufacturers may decide that it is cheaper to keep production facilities where they are and just absorb the tariff within operating costs and perhaps hope that the Administration’s attitude softens.

It will also raise substantial tax revenue thanks to a lack of US-made products that producers and consumers can substitute for. This gives President Trump the fiscal headroom to deliver on his promises for extended and expanded tax cuts later this year. As manufacturers reshore, tariff revenue will obviously decline, but the hope is that this will be more than offset by higher payroll and corporation tax receipts.

Nonetheless, the transition period will be painful with squeezed consumer spending power and corporate profits risking a weaker economy for 2025.

Cost pressures inevitably rise

President Trump claimed on multiple occasions that “foreigners will pay” the tariffs, despite the importing company paying the tax when it arrives at a US port. The Administration’s argument goes that if the dollar appreciates by the same amount that the tariff is levied at, they offset. This leaves foreigners paying through a loss of purchasing power via a weaker currency versus the USD.

In an environment where the dollar is weakening, like we’re seeing now, this clearly doesn’t work. It means sharply higher costs for US importers unless they can convince foreign producers to cut their prices meaningfully, or the dollar will rapidly strengthen once again. If not, the choice will be some combination of smaller profit margins for US companies and passing higher costs onto the US consumer.

US companies could choose to use US-made products instead of importing foreign goods, but this is not going to be possible for everything. The US imported $3.3tn worth of goods in 2024, yet the total value-added of US manufacturing as measured within the GDP report was just under $3tn. Therefore, the US manufacturing sector would need to more than double in size to remove the need for any imports. While that suggests huge scope for manufacturing expansion via reshoring, it can’t be achieved overnight so price increases through the supply chain are inevitable.

Price hikes of $1,350 per American look probable

In a worst-case scenario where there is no substitution for US-made products and there is 100% pass-through of the tariff to the consumer, we estimate US price levels will rise by 3.3%.

Total consumer spending was $19.83tn last year so if the roughly $600bn of tariff is passed fully through that expenditure would have totaled $20.49tn, which is 3.3% higher. Another way of thinking about it is that household disposable (after tax) income was $22.1tn in 2024, so $600bn of extra taxes is equivalent to 2.7% of disposable income. Spread evenly, that would be close to $1800 for every American, or $7200 for a family of four.

We know that when washing machines were subject to a 20% US tariff in 2018, around 60% of the tariff was initially passed onto the consumer based on the numbers published within the consumer price report. However, in 2018, it was on one specific product and importers and retailers may have taken the view that they could afford to absorb some of the cost as they would still be making ample profits on other products. When the tariff is on everything, that will not be as easy, hence why we suspect it is more likely to be a 75% pass-through to the consumer this time around. That would imply price levels more likely rising by around 2.5% or $1350 of extra cost for every American.

That may just be the start. There is also likely to be upward pressure on some services prices. For example, if cars and car parts and durable goods are more expensive then repair costs go up and vehicle and home insurance costs will rise too to cover future potential payouts.

Tariffs are regressive and will intensify the financial pressure on low-income households

The greater dollar tariff revenue figure will come from higher cost durable goods such as cars, which is likely to mean higher income households pay more than the average person – for example the top 20% of households by income account for 74% of new vehicles and parts purchases by value. For a typical vehicle, tariffs could add an extra $8000 to the purchase price so one way to mitigate the pain is to wait longer before buying a new vehicle.

However, in general tariffs are a regressive form of taxation with lower income households spending more of their on income on goods, which face tariffs – food, energy, clothing, household goods – whereas higher income households spend more on services – travel, recreation etc, which aren’t subject to tariffs.

We already know that consumer bifurcation is an important theme in the US. The top 20% of households by income are in great shape – they earn $200k+, have seen their asset base (property and stocks) surge in value and high interest rates have benefitted them – they typically own their property outright or are locked in at low mortgage rates and can put their cash in money market funds. The bottom 60% are feeling much more stress. They earn $90k and below (it falls away very quickly with a long tail) and are more likely to be in the 38% of households that rent, the cost of which has shot higher in recent years. They don’t have anywhere near as many assets, so haven’t benefited from rising property and stock markets and high borrowing costs hurt as they are the people that borrow on credit cards, car loans, etc.

Tariffs are only going to make the bifurcation worse. Financially pressured households will be cutting back spending in some areas to afford higher prices of essentials. It will also likely mean rising consumer loan defaults in an environment where Philadelphia Fed data shows a record high 10.5% of credit card holdings are only able to afford the minimum payment on their monthly credit card bill.

US business wary of foreign retribution

It isn’t just domestic demand that we are worried about. Foreign governments look set to implement reciprocal tariffs that hurt the price competitiveness of US-made products in those markets. In 2024, the US exported around $2.1tr of manufactured goods, the largest categories being automotive and parts ($169bn), civilian aircraft, parts and engines ($124bn), pharmaceuticals ($107bn).

Further complicating the situation are concerns about foreign consumer boycotts tied to both tariffs and President Trump’s other policy aspirations, including absorbing Canada and Greenland into the US, withdrawal of support for Ukraine and perceived support for Russia. Importantly, this can be much broader than purely a manufacturing story, such as reports of 70% declines in flight bookings from Canada, which will have knock-on effects for hotels and other service providers.

Tariffs, austerity and fears of job cuts heighten stagflation concerns

It wasn’t meant to be this way. The US economy was in a healthy position late last year with output growing at a near 3% rate, unemployment was low, the Federal Reserve had just cut its policy rate 100bp and equity markets were at all-time highs. President Trump’s election victory, it was thought, would see him come in and turbo charge the growth story by cutting taxes and slashing regulations.

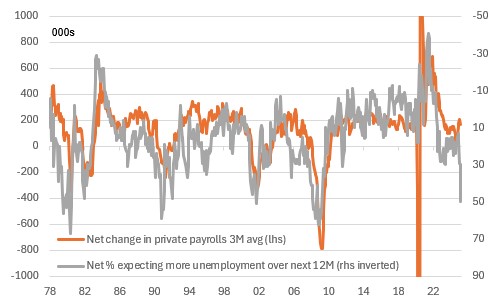

However, his focus on immigration, austerity and trade protectionism is instead leading to fears of stagflation. The chart below shows the respondents ’ views on where the jobs market is heading. That does not look a pretty picture and when overlayed with squeezed spending power and tighter profit margins amidst an environment of cooling asset prices, suggests downside risks for growth this year.

Households are increasingly pessimistic regarding job prospects

The Fed will be in a quandary. It will want to support the economy with rate cuts, but uncertainty over how long inflation may persist is likely to lead them to hesitate. We continue to forecast September and December rate cuts with a third in March 2026, but the gloomier near-term outlook for the economy means the risks are skewed to them having to do more this year.

Is Donald Trump for turning?

The key question is, will Donald Trump reverse course if the economic pain becomes too much? The problem is, he has invested so much in tariffs. Correcting perceived unfair trade practices and reshoring US manufacturing was always going to be a long-term goal given the cost and planning involved. His near-term need for the tariff revenues to give him the fiscal room to extend and expand his 2017 tax cuts also suggests he is not going to back down swiftly. Moreover, his team have been willing to acknowledge the risk of near-term pain for longer-term gain.

President Trump will be wary of the electoral calendar, though. Last night’s Florida congressional and Wisconsin state Supreme Court election results provided a warning shot, and the more economic pain the country faces, the more likely it is that the Democrats sense that they could regain control of the House of Representatives after next year’s mid-term elections. He may well gamble major tax cuts for 2026 will give him the boost he needs to get his party over the line and he can point to re-shoring announcements as “big wins” that allow him to pull back many of the tariffs. However, that will do little to address near-term fears of falling output, rising unemployment, elevated inflation and stressed financial markets.

Written by James Knightley, Chief International Economist, US

Shared by Golden State Mint on GoldenStateMint.com