Summary

- Stocks rallied in advance of Trump’s new trade deal, which proposes reciprocal tariffs that could severely impact the economy if implemented long term.

- The proposed tariffs, averaging 22-29%, could lead to the highest rates in over a century, risking a consumer-led recession and negating tax cut benefits.

- Lower- and middle-income consumers would be the hardest hit, with significant increases in household costs, making the policy economically unsustainable.

- The tariff policy is likely temporary due to implementation challenges and market reactions, with potential reductions or rescindments expected within 30–60 days.

- This idea was discussed in more depth with members of my private investing community, The Portfolio Architect.

Punnarong/iStock via Getty Images

Stocks rallied for a third day in a row after testing the correction low in the S&P 500 on Monday morning. We are going to retest that low this morning for a second time, and my hope is that it holds once investors recognize the art of President Trump’s newly proposed deal on trade. Unfortunately, what investors are trading is one uncertainty for another in a grand experiment to reshape the global economy. While the actual policy is no longer uncertain, how long it stays in place and what it ultimately looks like remains to be seen. In after-hours trading, stocks briefly soared when the president announced that our trading partners would face a reciprocal tariff rate that is half of what they charge us, with a 10% minimum. That was far more reasonable and less punitive than the 20% tariff feared, which was viewed as a worst-case scenario. Then an explanation of what reciprocal means was provided, and stock market futures plunged.

Finviz

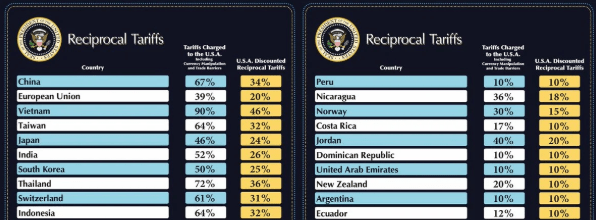

According to the president, the reciprocal rate considers not just the tariff foreign countries charge but also includes the Trump administration’s calculation of currency manipulation and other non-monetary barriers. That is how they arrived at a 34% rate on imports from China, and a 46% rate on imports from Vietnam, among 183 other countries, but these percentages look more like an arbitrary back-of-the-napkin calculation in order to arrive at a specific amount of tax revenue. This is obviously far more Draconian than anyone could have imagined, and if implemented and permanent through the end of this year, would surely hurl the US economy into a consumer-led recession. This is why I think the president’s proposal is a more aggressive negotiating tactic to force concessions, but the art of his approach risks further damaging sentiment and testing the patience of consumers who are already anxiety-struck about higher prices. These new deals need to happen quickly before the weight of these tariffs impacts economic activity.

Bloomberg

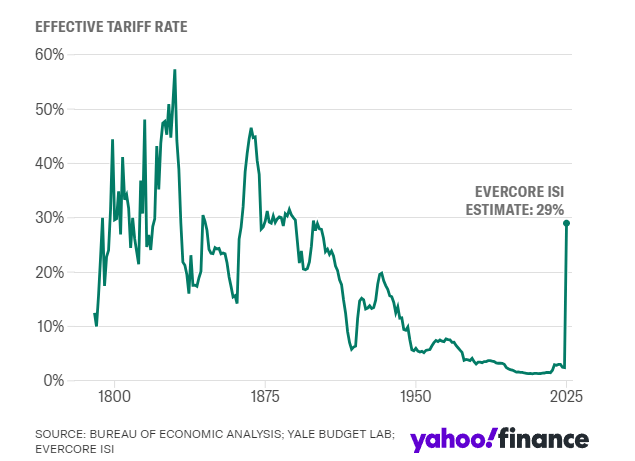

Early estimates on Wall Street indicate the average tariff rate on more than $3 trillion of imported goods will be in a range of 22-29%. It would be the highest tariff rate in more than 100 years, exceeding the 20% rate implemented after the Smoot-Hawley Tariff Act of 1930, which was an abysmal failure. It would be the largest tax increase in history and raise more than $600 billion on an annualized basis from the pockets of US businesses and consumers, which is clearly untenable. Not to mention the impact retaliatory measures by our trading partners would have on our exports, including the outright boycott of goods. It would also completely negate the benefits of promised tax cuts later this year. This is why I see it as an extremely aggressive negotiating tactic because the policy is not economically viable for any meaningful length of time.

Yahoo

Lower- and middle-income consumers would be hit the hardest under this trade policy because tariffs are a regressive consumption tax in that lower-income households spend a larger percentage of their income on goods and services. This would adversely impact a large swath of the president’s base. The Yale Budget Lab estimates a 20% duty on all imports would cost the average household between $3,400 and $4,200 a year in lost buying power from price increases. The Tax Foundation says the amount would be closer to $2,000. Regardless, no pundits see prices falling, and consumers were expecting an end to inflation and not its resurgence. This is one reason I do not think this policy, as proposed, can be sustained for very long.

The second reason is that we don’t have the manpower or the infrastructure to implement it. Consider that when President Trump doubled the tariff on Chinese imports from 10% to 20% and suspended the de minimis provision that allowed packages worth less than $800 to enter the US tariff-free in early February, the customs department imploded. Approximately 80% of the nearly four million packages that are imported from China each day are valued at less than $800. Customs and Border Protection is not capable of handling this volume, which is why the Trump administration delayed the suspension days after implementing the new tariff rate. Experts contend that it would take at least a year to set up a system to account for this volume.

Once again, the Trump administration’s new tariff regime ends the de minimis provision. How are customs officials going to suddenly process this volume on top of new and varied tax rates on more than $3 trillion in goods from 185 countries? If it happens at all, it won’t happen any time soon. Most importantly, this suggests consumers and businesses won’t see the full impact of these price increases for months.

For these two reasons, I don’t think the Trump administration’s new tariff policy will remain in place for very long. I give it 30–60 days before rates are reduced or rescinded under the auspices of concessions or better trade deals. Furthermore, the financial markets are clearly not going to cooperate with the president. A strong dollar was supposed to be an offset to the headwinds of protectionism. Instead, the dollar is plunging. Treasury Secretary Scott Bessent asserted that if we have good policies, the stock market will outperform. On the contrary, the US is one of the worst-performing markets in the world this year.

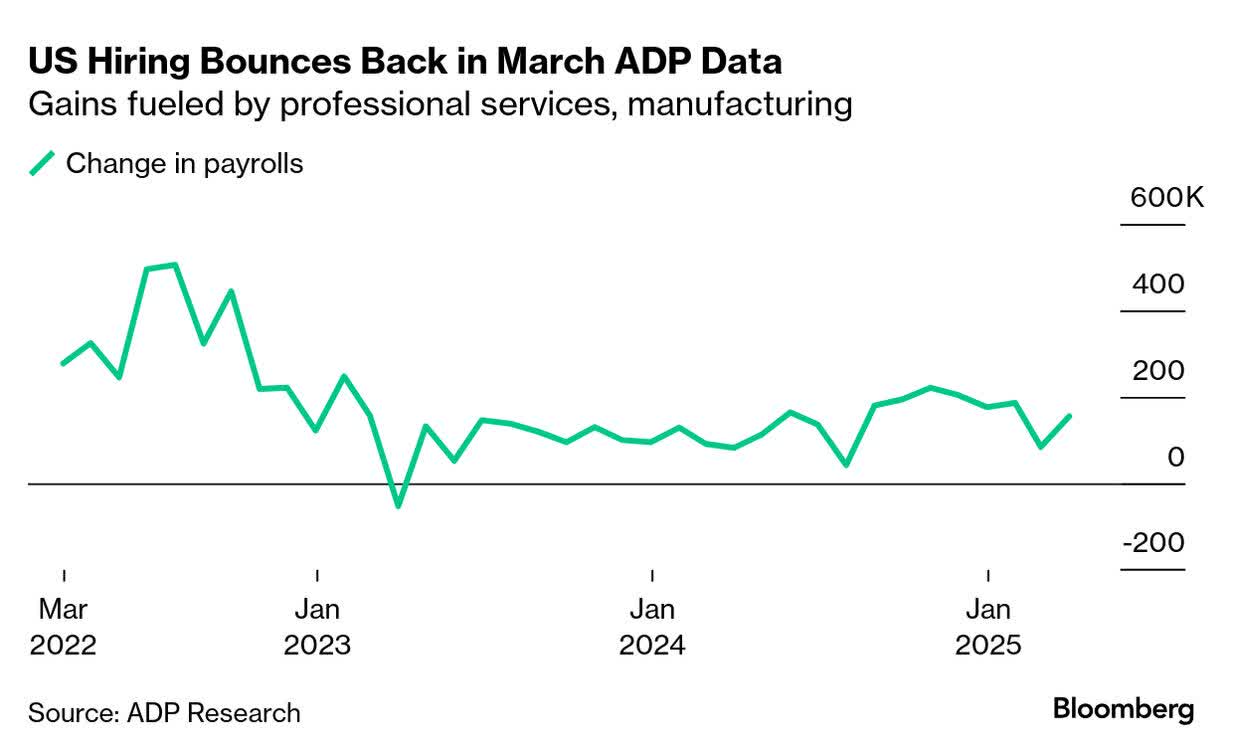

The good news, if any can be found, is that the real economy is still performing in line with the soft landing scenario I expected at the beginning of this year. Despite the tariff turmoil, hiring in the private sector remained robust in March with ADP reporting that the economy added 155,000 jobs, which was a meaningful increase from the 84,000 in February. This doesn’t surprise me because the service sector survey from S&P Global showed a sharp increase in business activity in March. Consumer spending is clearly a lot stronger than sentiment surveys suggest, and spending is what leads to job growth.

Bloomberg

The one caveat is that if today’s downdraft in stock prices is the beginning of a more meaningful decline than the correction we just had, it can lead to a negative wealth effect. A deeper and more prolonged drawdown in markets is likely to slow the rate of consumer spending growth beyond what should be expected during a mid-cycle slowdown. We have not seen that yet. If we can successfully retest Monday’s low and find some firmer ground in the days ahead, that should help sentiment. Again, this is a market event and not yet an economic one, but the president is going to have to move quickly to keep that from happening.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Lawrence Fuller is the Principal of Fuller Asset Management (FAM), a state registered investment adviser. He is also the manager of the Focused Growth portfolio on the copy-trading platform Dubapp.com. Information presented is for educational purposes only intended for a broad audience. The information does not intend to make an offer or solicitation for the sale of purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. FAM has reasonable belief that this marketing does not include any false or material misleading statements or omissions of facts regarding services, investment, or client experience. FAM has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Past performance of specific investment advice should not be relied upon without knowledge of certain circumstances or market events, nature and timing of investments and relevant constraints of the investment. FAM has presented information in a fair and balanced manner. FAM is not giving tax, legal, or accounting advice. Mr. Fuller may discuss and display charts, graphs, formulas, and stock picks which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions. Consultation with a licensed financial professional is strongly suggested. The opinions expressed herein are those of the firm and are subject to change without notice. The opinions referenced are as of the date of publication and are subject to change due to changes in market or economic conditions and may not necessarily come to pass.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Shared by Golden State Mint on GoldenStateMint.com