By James Knightley

By James KnightleyConsumer resilience continues

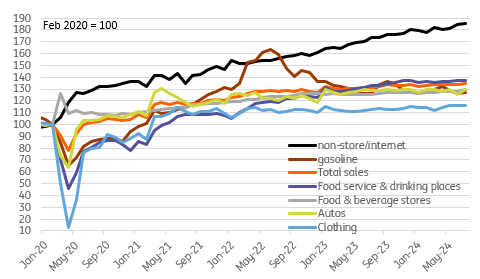

The initial wave of today’s US data was quite a bit firmer than expected with retail sales rising 1% month-on-month versus the 0.4% consensus with the control group, which excludes some of the volatile items, seeing sales rise 0.3% MoM versus expectations of a 0.1% gain. There were some downward revisions to the history, but this is still a firmer-than-anticipated outcome.

The headline figure was boosted by a 3.6% MoM jump in vehicle sales, but there was also decent strength in electronics (+1.6%), building materials (+0.9%), food & beverage (+0.9%) and health/personal care (+0.8%). These gains more than offset weakness in miscellaneous stores (-2.5%), sporting goods (-0.7%), department stores (-0.2%) and clothing (-0.1%). We had been thinking the risks were skewed to the downside on the basis that the June control groups gain of 0.9% was vulnerable to a correction after hot and humid weather across the US boosted traffic at shopping malls. This resilience in consumer spending gives enough excuse to push the market to increasingly favor a 25bp Fed interest rate cut over a 50bp move in September.

US retail sales levels

Source: Macrobond, ING

Jobless claims show lay-offs remain low

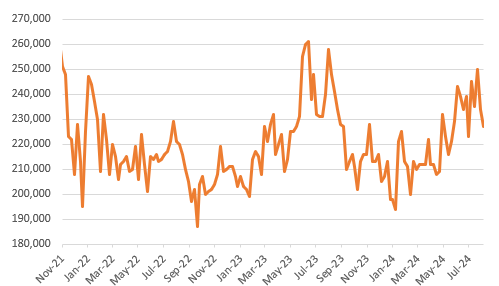

Meanwhile, jobless claims surprisingly moderated to 227k from 234k (consensus 235k) with continuing claims dipping to 1864k from 1871k (consensus 1870k). This is the second consecutive slowing in initial jobless claims and is the lowest number since the first week of July. As such it reinforces the message that the rise in the unemployment rate is being caused by increased labor supply exceeding labor demand rather than job lay-offs, which again points to a greater chance of a 25bp cut than a 50bp move that we had penciled-in in the wake of the jobs report.

Weekly initial jobless claims

Source: Macrobond, ING

Industrial production remains subdued

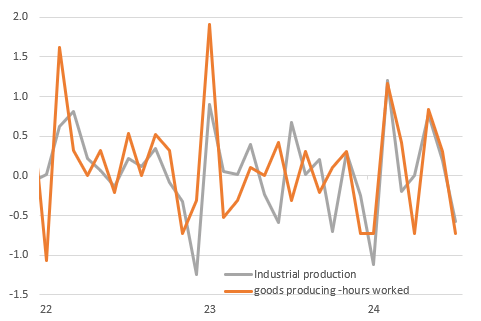

Rounding out the main US numbers, we have industrial production falling 0.6% MoM with June’s growth rate revised down to +0.3% from an initially reported +0.6% gain. Hours worked in the sector are the best guide for output growth and the fact they fell 0.6% indicated downside risk to the consensus forecast of a 0.3% decline. Hurricane Beryl played a major part of this as it disrupted the Gulf Coast. The ISM manufacturing index remains in contraction territory and weak orders levels point to a sector that will continue to struggle. Nonetheless, the US economy is dominated by services these days and that remains in a stronger position, for now.

MoM change in industrial output and the hours worked in the sector

Source: Macrobond, ING

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.

Shared by Golden State Mint on GoldenStateMint.com