(Bloomberg) — Bond yields fell as a big downward revision of US payrolls reinforced bets the Federal Reserve will cut rates in September.

(Bloomberg) — Bond yields fell as a big downward revision of US payrolls reinforced bets the Federal Reserve will cut rates in September.Treasuries rose across the curve, with the move led by shorter maturities. Swap traders are pricing in about 100 basis points worth of easing in 2024. The implied rate on the contracts show traders expect a quarter-point cut next month — and a roughly 20% chance for a half-point reduction. Equities fluctuated.

While the annual revision to US jobs growth isn’t something that would usually impact trading, it got attention this time around due to the recent concern the labor market is cooling too much amid elevated Fed rates.

US job growth was probably far less robust in the year through March than previously reported. The number of workers on payrolls will likely be revised down by 818,000 for the 12 months through March — or around 68,000 less each month. It was the largest downward revision since 2009.

“The main message from the revisions in my mind is reinforce just how ‘silly’ it is to let the next jobs number be the determinant in whether to go 25 or 50 in September,” said Neil Dutta at Renaissance Macro Research. “What this revision data imply is that whatever the next jobs number is going to be, it’s probably lower in reality.”

Jamie Cox at Harris Financial Group says that “if you are in the rate cut in September camp, these data all but ‘seal the deal’ on what Fed needed to cut rates.”

In the run-up to Jerome Powell’s Friday speech in Jackson Hole, traders will scour minutes from the latest Fed policy meeting on Wednesday. Any clues on the path ahead for rates will be in focus, as well as any guidance on when the Fed will complete its current course of quantitative tightening.

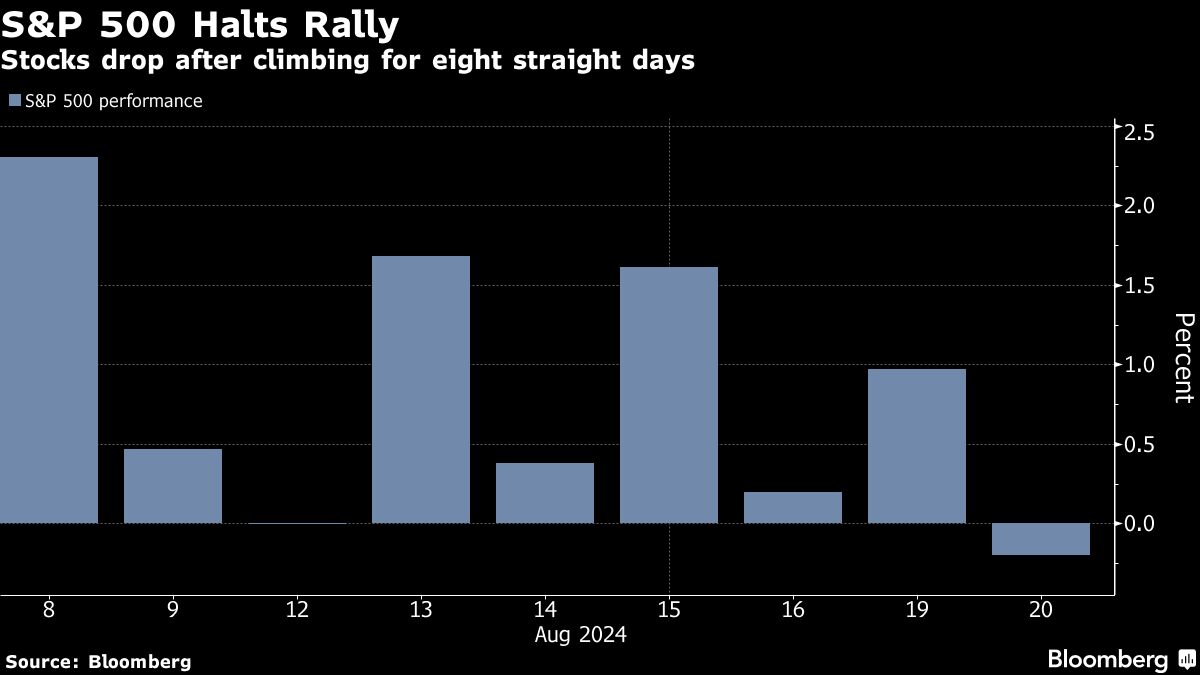

Treasury 10-year yields declined three basis points to 3.78%. The S&P 500 hovered near 5,600. Target Corp. climbed 12% after ending a string of sales declines in the second quarter, citing improved discretionary spending. Macy’s Inc. slightly missed estimates for its quarterly revenue and lowered its outlook for sales during the rest of the year.

Krishna Guha at Evercore says the big payroll revisions will reinforce the Fed’s assessment that the labor market has been softening under restrictive policy and that it will need to recalibrate rates in a timely manner to prevent this from extending further than desired.

All this favors a relatively “low bar” for 50 basis-point rate cuts. The base case remains a string of 25 basis-point moves.

“We are confident this will be the takeaway from Powell at Jackson Hole Friday,” Guha noted. “But in the interim, we suspect minutes from the July meeting may well feel ‘hawkish-stale.’ A lot has happened since then.”

At Strategas, Don Rissmiller says the case for lower policy rates got stronger. The Fed will need to validate this rate cut cycle – which likely means multiple cuts, he noted, pointing to Powell’s speeech on Friday at Jackson Hole.

To Jennifer McKeown at Capital Economics, central bankers are unlikely to offer much forward guidance at the Jackson Hole symposium, preferring to stress their “data dependence”.

“Since most economies are expanding, inflation is easing back to target and financial markets have stabilized after the recession scare a few weeks ago, there is less pressure for them to steer markets than there has been around past events,” she noted. “But they risk keeping rates too high for too long.”

With the Fed poised to cut interest rates from restrictive levels and still strong economic and earnings fundamentals, the the environment remains supportive for stocks, with still strong economic and earnings fundamentals, and a Fed poised to cut interest rates from restrictive levels, according to Solita Marcelli at UBS Global Wealth Management.

“Our base-case year-end and June 2025 S&P 500 price targets remain 5,900 and 6,200, respectively.”

Marcelli believes quality growth remains well placed to outperform. Firms with competitive advantages and exposure to structural drivers should be better positioned to grow and reinvest earnings consistently, she noted.

“The volatility from the past month has settled, as macro fears subside, expectations were reset, and investors used the weakness as an opportunity to add to risk exposure,” said Mark Hackett at Nationwide. “The next catalyst for markets is Fed data, including the minutes from the FOMC meeting and the Jackson Hole speeches. This likely results in a wait-and-see approach until Friday.”

Corporate Highlights:

- Ford Motor Co. is recalibrating its electrification strategy yet again, canceling plans for a fully electric sport utility vehicle in a shift that may cost the carmaker around $1.9 billion.

- Walmart Inc. raised about $3.6 billion by selling its stake in Chinese e-commerce firm JD.com Inc., winding down an eight-year partnership that appears to be paying diminishing returns amid a challenging landscape for Chinese tech giants.

- US coal producer Consol Energy Inc. agreed to merge with Arch Resources Inc. in a $2.3 billion deal as the transition to greener fuels threatens the industry’s long-term outlook.

- Brookfield Asset Management is asking banks to line up about €9.5 billion ($10.6 billion) of debt for its potential take-private deal for Spanish pharmaceutical producer Grifols SA, according to people with knowledge of the matter.

Key events this week:

- Eurozone HCOB PMI, consumer confidence, Thursday

- ECB publishes account of July rate decision, Thursday

- US initial jobless claims, existing home sales, S&P Global PMI, Thursday

- Japan CPI, Friday

- BOJ’s Kazuo Ueda to attend special session at Japan’s parliament to discuss July hike, Friday

- US new home sales, Friday

- Jerome Powell speaks in Jackson Hole, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.1% as of 12:24 p.m. New York time

- The Nasdaq 100 rose 0.1%

- The Dow Jones Industrial Average was little changed

- The MSCI World Index rose 0.2%

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro rose 0.1% to $1.1146

- The British pound rose 0.4% to $1.3081

- The Japanese yen rose 0.1% to 145.10 per dollar

Cryptocurrencies

- Bitcoin rose 0.5% to $59,592.77

- Ether rose 0.5% to $2,602.99

Bonds

- The yield on 10-year Treasuries declined three basis points to 3.78%

- Germany’s 10-year yield declined two basis points to 2.19%

- Britain’s 10-year yield declined two basis points to 3.89%

Commodities

- West Texas Intermediate crude fell 1.3% to $72.24 a barrel

- Spot gold fell 0.4% to $2,504.93 an ounce

©2024 Bloomberg L.P.

Shared by Golden State Mint on GoldenStateMint.com